What should the Bank of Japan do with its huge stock portfolio?

What should the Bank of Japan do with its huge stock portfolio?

Financial Times

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is an FT contributing editor

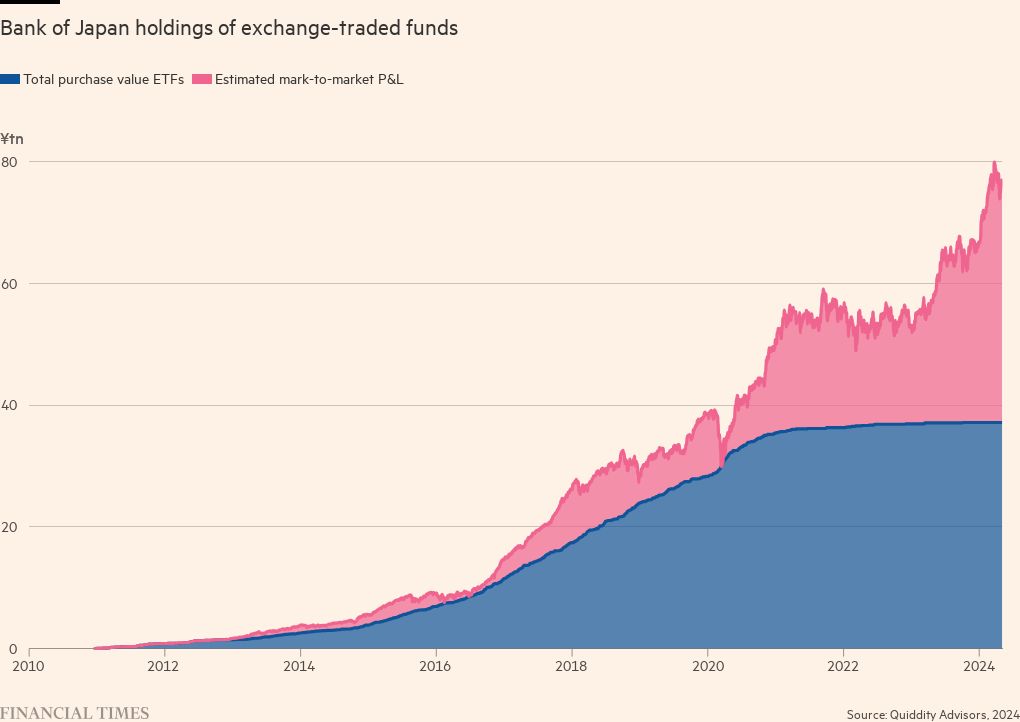

The Bank of Japan has, over 14 years, acquired exchange-traded funds containing stocks equivalent to about 7 per cent of listed Japanese firms. In March, BOJ governor Kazuo Ueda called time on this aspect of the central bank’s extraordinary monetary easing programme. The bank has yet to announce what it will do with its half-a-trillion-dollar stock portfolio.

But with about a quarter of stock market gains during the Abenomics period connected to their stock buying, a poorly managed exit could sink the Japanese equity market. It could also undermine the BoJ’s inflation objective.

Why exit at all? After all, in a world of gaping losses from quantitative easing programmes by central banks to support economies, the BoJ’s ETF portfolio has delivered a rare profit. The ¥37tn of cumulative stock purchases have ballooned in value to be worth an estimated ¥77tn today, according to some estimates. Criticism that individual stock prices were being distorted has largely faded since the BoJ reduced the cost of stock-borrowing. And, as Naohiko Baba, head of Japan research at Barclays, notes, the roughly ¥1.2tn in dividends that they bring come in handy. It’s enough to defray the cost of policy normalisation of its monetary policy, offsetting the cost of interest on reserves held at the bank on a policy rate up to at least 0.25 per cent.

But the bank isn’t a natural holder of stock. Its accounting framework is penal. Unrealised stock losses must be provisioned, but unrealised gains are never recognised. As such the balance sheet has an asymmetric vulnerability to stock price volatility.

So what are Ueda’s possible exit ramps? First up, the Bank of Japan itself has form. Ahead of, and during, the global financial crisis the Bank bought around ¥2.4tn in shares held by financial institutions. After initial abortive attempts, these have been in steady liquidation since 2016.

The market impact has gone almost unnoticed, but the pace has been glacial. The BoJ could apply the same softly-softly practice to ETF sales. But this would take roughly two-and-a-half centuries to complete at the same pace. Ueda has indicated he’s in no hurry but this may be stretching things.

You are seeing a snapshot of an interactive graphic. This is most likely due to being offline or JavaScript being disabled in your

The full article is available here. This article was published at FT Markets.

Comments are closed for this article!