The increasingly blurred lines between banks and NBFIs

The increasingly blurred lines between banks and NBFIs

Financial Times

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Once upon a time, banks were bigger than non-bank financial institutions (NBFIs). Those days are now a dim and distant memory. The blame (or credit) for this is usually laid at the door of regulators.

One justification for regulating banks much more heavily than NBFIs is that they matter more. Banks do different things (like take deposits) and can’t be allowed to fail. NBFIs – like mutual funds, pensions and insurance firms – can die without summoning the end of days. Or so one view goes.

Another perspective on NBFIs is that they are sneaky critters, which creep around regulatory perimeters and eat banks’ lunches. Think pesky private credit funds that lend to firms, mutual funds that buy corporate bonds, etc. In this characterisation, NBFIs will have to be rescued, from time to time, when they blow up.

In both worlds NBFIs sort of run in parallel with the banking system as an under-regulated little big brother. And at the very least they add diversification to the financial ecosystem. But do they? These are the questions tackled by Viral Acharya – former deputy governor of the Reserve Bank of India, and now of NYU – Nicola Cetorelli of the FRBNY, and Bruce Tuckman of NYU. Their answer became the keynote paper at a Riksbank conference last year we’ve only just landed upon (h/t Usama Polani).

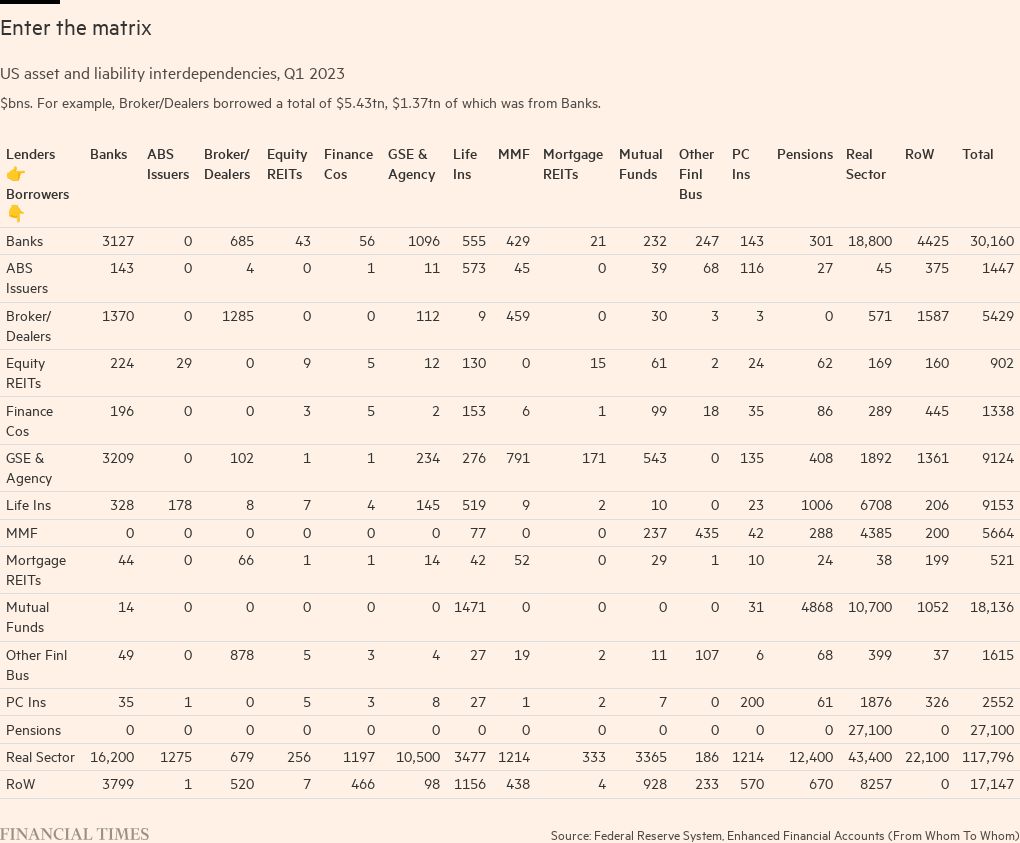

Using new(ish) and enhanced financial accounts data for the United States, they find that — rather than NBFIs substituting for bank business — NBFI and bank businesses and risks are better seen as increasingly interwoven.

The authors run through a bunch of examples of this interdependence, which will be familiar to some regular readers. These range from the sale of $2.3bn of loans from PacWest to Ares via Barclays in the regional bank crisis of March 2023, Blackstone Private Credit Fund’s 19 secured credit commitment facilities, REITs’ use of bank credit lines as warehouse financing, European electricity producers’ derivative use, to the UK’s very own pensions LDI crisis.

They present their findings as a big ol’ table at the back of their paper, which we’ve recreated here:

You are seeing a snapshot of an interactive graphic. This is most likely due to being offline or JavaScript being disabled in your browser.

Maybe you enjoyed that but if, like us, tables cause your eyes to glaze

The full article is available here. This article was published at FT Markets.

Comments are closed for this article!