Low volatility shows investors are underpricing risk

Low volatility shows investors are underpricing risk

Financial Times

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is chief economic strategist at Netwealth

Are financial markets pricing sufficiently for future risks? Measures of financial market volatility suggest not.

There are different measures of market volatility. Occasionally, they move the same way. This is often countercyclical, when the economic environment is stable and the political and policy outlook is clear and predictable.

Shocks, likewise, can have a similar effect, usually triggering rising volatility. Then the policy response may lead asset classes to behave differently, both in direction and volatility.

What about now? Volatility across equity and currency markets is low. The most widely followed gauge of equity market volatility expectations is the Vix. Its value of 12.46 compares with an average over five years of 21.5 and over the longer-term of 19.9.

Increased issuance of yield-enhancing structured investment products and their greater use by option dealers has reinforced the low value of the Vix. Notwithstanding this, other measures such as standard deviations in market moves confirm low volatility. The fall in inflation since 2022 has been the main driver. Equity markets, it seems, are discounting good news and a disinflationary environment.

More remarkable, perhaps, is low volatility across currency markets. The DB index of foreign exchange volatility captures the picture. It is at 6.3 versus an average of 7.6 over five years and 9.3 over the longer term. This is despite bouts of volatility associated with a competitive weakening of the yen, renminbi and won.

However, low currency volatility may discourage hedging, undermine market depth and resilience. Low volatility and tight spreads in credit interest rates over benchmarks have also been evident in corporate bond markets, despite higher refinancing costs and defaults.

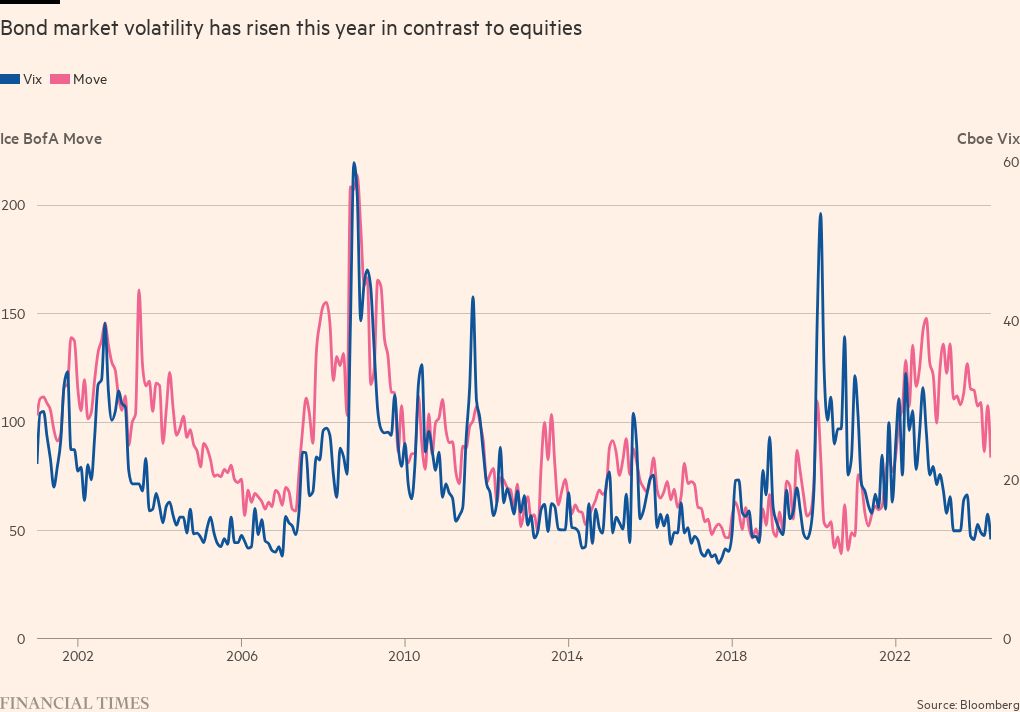

In contrast, volatility in bond markets has risen this year. The ICE BofA Move index of volatility in US Treasuries is at 83.6, just below both its five-year and longer-term averages. This is explained by the market’s shift away from expectations of a large number of rate cuts in the US.

As policy rates fall, bond market volatility should ease, perhaps temporarily. But the challenge is that many of the assumptions underpinning low volatility across markets may be subject to challenge. Not least is how the juncture of political, geopolitical, policy and economic risks are likely to align.

Take inflation. Inappropriate monetary policy and supply-side shocks led inflation to persist. A key driver of low global

The full article is available here. This article was published at FT Markets.

Comments are closed for this article!