Daiwa stake in Aozora could help in the battle of Japan’s brokers

Daiwa stake in Aozora could help in the battle of Japan’s brokers

Financial Times

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

In Japan, Nomura is hard to beat. Japan’s largest brokerage house has a market share of about a third at home. That is more impressive if you consider how fragmented the market is, with more than 200 competitors.

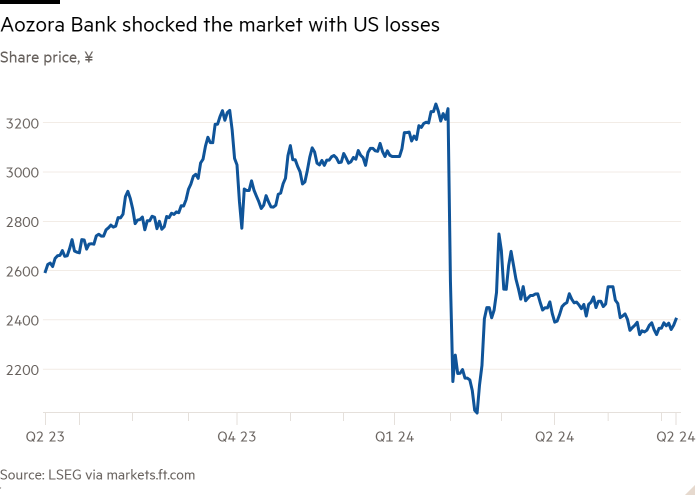

Of them, Daiwa Securities is a strong runner-up. But bridging the gap with Nomura has long seemed a tall task. Its latest effort — taking a big stake in Aozora, Japan’s worst-performing major bank stock — went down badly. Daiwa shares fell nearly 5 per cent on Tuesday, despite the deal giving Daiwa a discount on its stake compared with the undisturbed price. This bet may not be as reckless as the market reaction suggests.

Daiwa, Japan’s second-largest brokerage house, has agreed to buy a stake in Aozora Bank — a mid-sized bank with a market value of $1.8bn — from a fund with ties to Yoshiaki Murakami, Japan’s most famous activist investor. This raises its stake in Aozora to 24 per cent.

The concern from Daiwa’s investors is understandable. Shares of Aozora have had a rollercoaster ride, after it posted its first loss in 15 years earlier this year. Large losses on its portfolio of US office property loans shocked its conservative retail investor base.

But Aozora’s history in the US commercial real estate and US agency bonds market is not necessarily a bad thing for Daiwa. Like local brokerage peers, Daiwa has a strong record in stable businesses such as mutual funds and wealth management. It has stuck to a conservative management style, similar to larger names such as Mizuho.

These brokers are starting to face unprecedented, intense competition from online brokers in Japan. The worry is that upstart online rivals have been undercutting each other to offer zero commission fees for cash and margin trading in Japanese stocks over the past year. A more aggressive shift in strategy is in order.

While the stock market reaction to Aozora’s loss was dramatic in February, US office loans accounted for less than a tenth of its total loan book. The sell-off was as much a reflection of how stable its performance has been since 2008 as it was of investor concern about its overseas business strategy. Its shares trade at just over 0.7 times tangible book value, a discount of about a quarter to local rivals

Daiwa will get an

The full article is available here. This article was published at FT Markets.

Comments are closed for this article!