US Economy Still On Track For Modest Pickup In Growth For Q2

US Economy Still On Track For Modest Pickup In Growth For Q2

The Capital Spectator

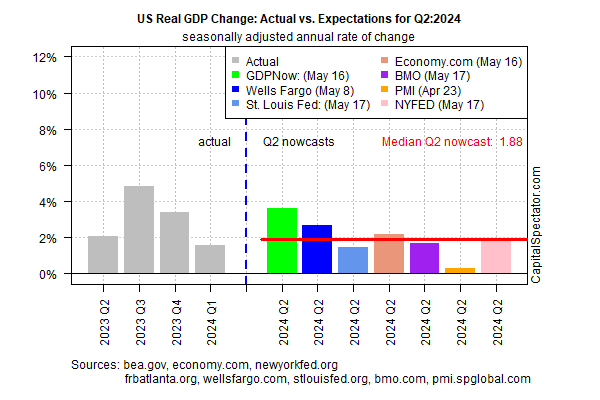

US economic activity is expected to post a modestly firmer increase in the second-quarter, based on the median estimate for a set of nowcasts compiled by CapitalSpectator.com. More than half of the quarter’s data sets have yet to be published, but the early clues continue to skew positive.

Output for the April-through-June period is projected to rise 1.9% (seasonally adjusted real annual rate), a modest pickup over Q1’s 1.6 advance. If the median Q2 nowcast is correct, the economy will post its first improvement over the previous quarter since the surge in output in 2023’s Q3.

With less than half of the quarter’s data set published there’s still a high degree of uncertainty about Q2’s outlook. But today’s update is encouraging in that the 1.9% nowcast for Q2 is essentially unchanged from the previous estimate (published on May 3).

Despite the relatively upbeat profile, there are several risk factors lurking, including negative sentiment. A new poll of Americans “wrongly believe the US is in an economic recession,” reports The Guardian.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Meanwhile, the US Consumer Sentiment Index weakened in May to its lowest reading in six months. “While consumers had been reserving judgment for the past few months, they now perceive negative developments on a number of dimensions,” reports Joanne Hsu, surveys of consumers director. “They expressed worries that inflation, unemployment and interest rates may all be moving in an unfavorable direction in the year ahead.”

It’s unclear how much of an impact that sentiment will have on the real economy, but it’s certainly a headwind in some degree. Nonetheless, today’s GDP nowcast suggests that the economy may be stabilizing if not firming up relative to Q1.

A possible early sign of trouble for later this year is the ongoing slowdown in labor market growth. Year-over-year private payrolls growth has ranged from 1.6% to 1.8% in recent months through April. A print below 1.6% in the upcoming May report would mark the slowest trend since the economy rebounded from the pandemic – a possible warning sign for the second half of 2024.

Meanwhile, retail sales growth has turned sluggish lately and so the May update will be widely watched.

For some economists, recession risk is already estimated as high for later this year. “Firms are hiring at a lower rate. Firms

The full article is available here. This article was published at The Capital Spectator.

Comments are closed for this article!